Nigeria's economy is growing too slowly to meet President Bola Tinubu’s ambitious goal of a $1 trillion GDP by 2030.

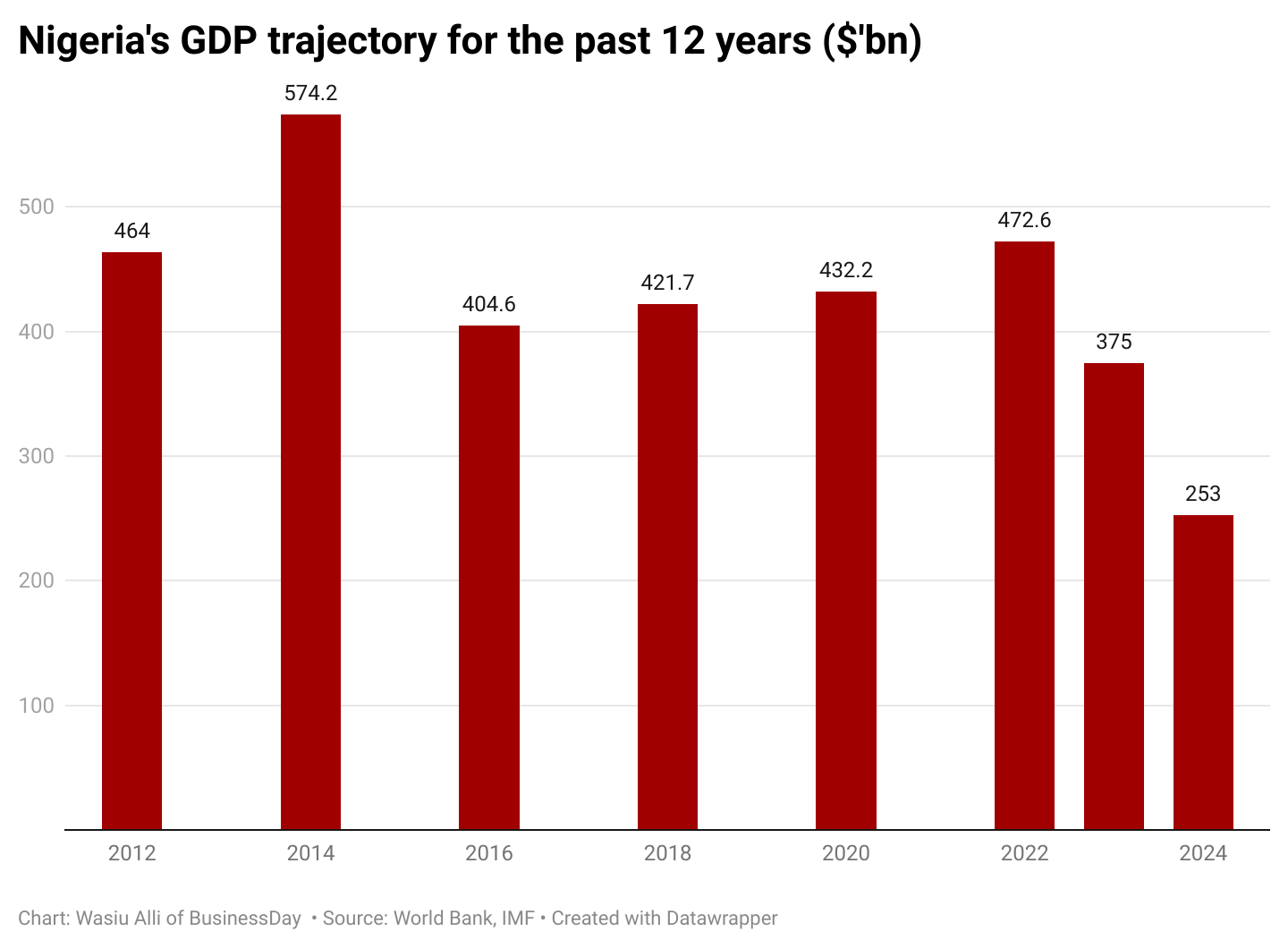

To attain this target Tinubu will have to steer a fumbling economy projected to be worth only $253 billion by the end of this year towards a four-fold surge.

He has started very slowly.

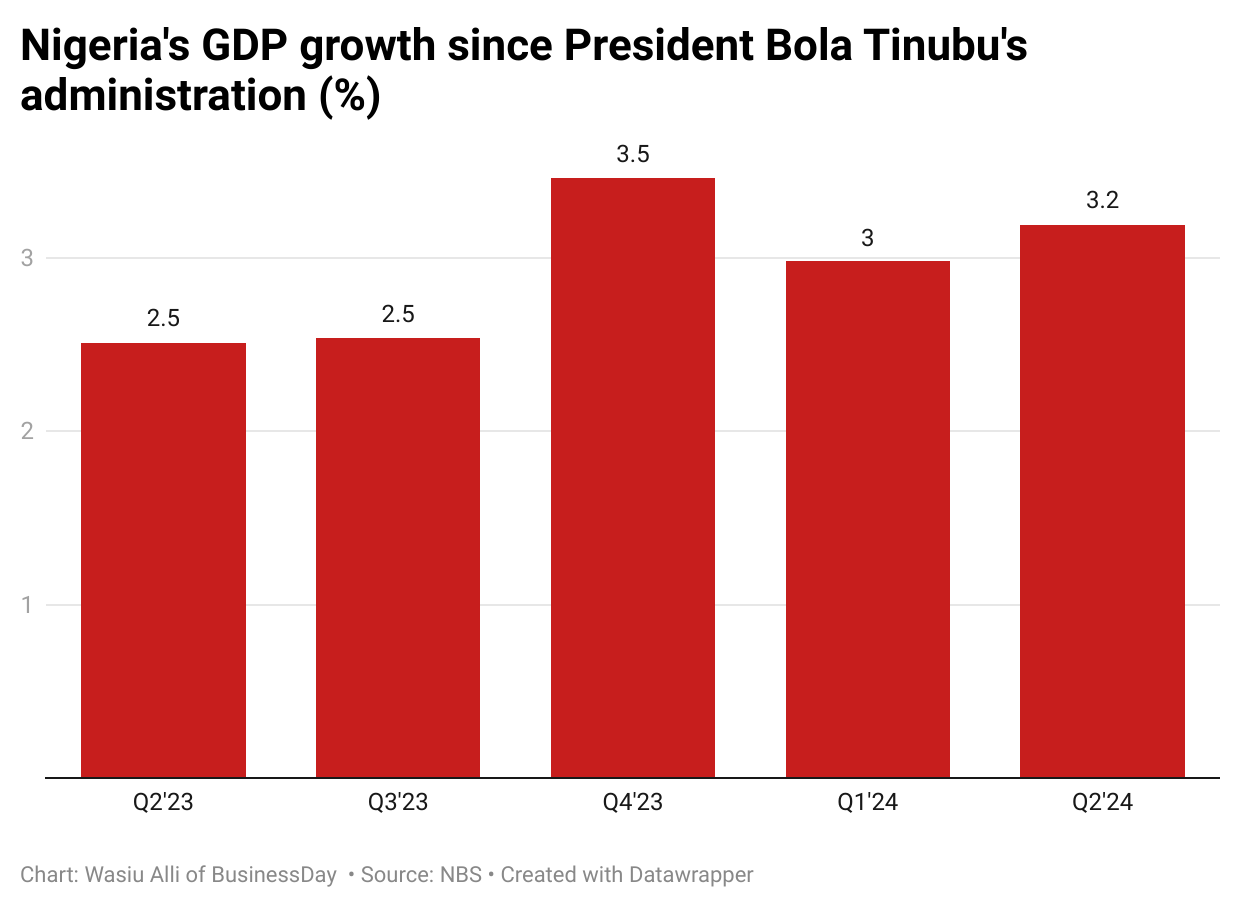

Nigeria’s highest quarterly GDP growth under Tinubu, who assumed office last May, came in the fourth quarter of 2023 at 3.5 percent with the most recent figure for the second quarter of 2024 showing the economy expanded by 3.19 percent.

The pace of growth will be insufficient to meet Tinubu’s $1 trillion economy target, according to economists polled by BusinessDay.

Ayo Teriba, chief executive officer of Economic Associates (EA) said the 3.1 percent growth in the GDP reported by the National Bureau of Statistics (NBS) is an “illusion” as the growth was measured in naira terms instead of dollars.

He added that the international benchmark for measuring a country's GDP is in dollars, calling on the authorities to “remove the naira veil to avoid implicit contradictions”.

“If you look at Nigeria's GDP over the last 10 years, it's been declining in dollar terms because the exchange rate has been weakening,” Teriba said, stressing that the country's economy could surpass the trillion dollar goal by ensuring stability in exchange rate.

“We need to build up our reserves aggressively to stabilise the exchange rate at about N150 - 160 to a dollar, which it was about 10 years ago, then a trillion dollars can be achieved even before six years,” the renowned economist said.

"I get am before, no be property"

Nigeria, once Africa’s largest economy, now ranks fourth behind South Africa, Egypt, and Algeria, with its GDP falling to $253 billion in 2024 from $477 billion in 2022, according to the International Monetary Fund (IMF).

South Africa now leads as Africa’s largest economy with a GDP of $373 billion, followed by Egypt with $348 billion, and Algeria with $267 billion.

Based on the IMF’s estimates, Nigeria’s GDP in US dollars declined from $477 billion in 2022, to $375 billion in 2023, and is estimated to drop to $253 billion in 2024.

However, in naira terms, the economy improved from N202.4 trillion in 2022 to N234.4 trillion in 2023. For 2024, the GDP is projected to hit N296.4 trillion.

The IMF had estimated that Nigeria’s GDP will grow by 3.34 percent in 2024 up from the 2.86 percent growth rate posted in 2023. But a weaker-than-expected growth saw the Washington-based Fund downgrade the country's economic growth to 3.1 percent.

CFG Advisory, a Lagos-based financial reporting firm, said in a report recently that GDP growth of “3 percent is not sustainable for our population of 200 million. Nigeria requires 8-10 percent GDP growth for sustainability.”

“Our GDP in nominal terms is $253 billion this year, 2024. And 2030 is just 6 years away. Meaning if we want to be a trillion dollar economy by then, we would need to increase our economic activity four fold,” said Samson G Simon, chief economist at ARKK Economics and Data Limited.

Nigeria needs to add $750bn in 6yrs to meet target

Simon further stated that for Nigeria to generate an additional $750 billion in six years to achieve a $1 trillion economy, it would mean adding $150 billion yearly on the average till 2030, culminating into a yearly growth of 60 percent.

The Abuja-based economist said that achieving a trillion dollar projection may be possible soon if Nigeria is made “the easiest place to do business.”

“Make it extremely attractive for Nigerians and non Nigerians alike to not only invest and do business here but also to retain the investments while ploughing back the proceeds within Nigeria,” Simon said.

“Doing this singular thing would be more than overarching for the Nigerian economy. Of course, this does not mean when this is done Nigeria would automatically attain the $ 1 trillion status. But doing it would make it more likely than doing anything else,” the economist added.

Muda Yusuf, the CEO of Centre for Promotion of Private Enterprises (CPPE), said the target of a trillion dollar GDP is not impossible, noting that the growth of a country's economy is as a result of the influx of investments.

“Some key sectors have the potential to grow very well, given their current levels of development. For instance, the agricultural sector needs to be transformed through mechanisation, commercial farming and technological integration. We are going to have a quantum leap in that sector,” he said.

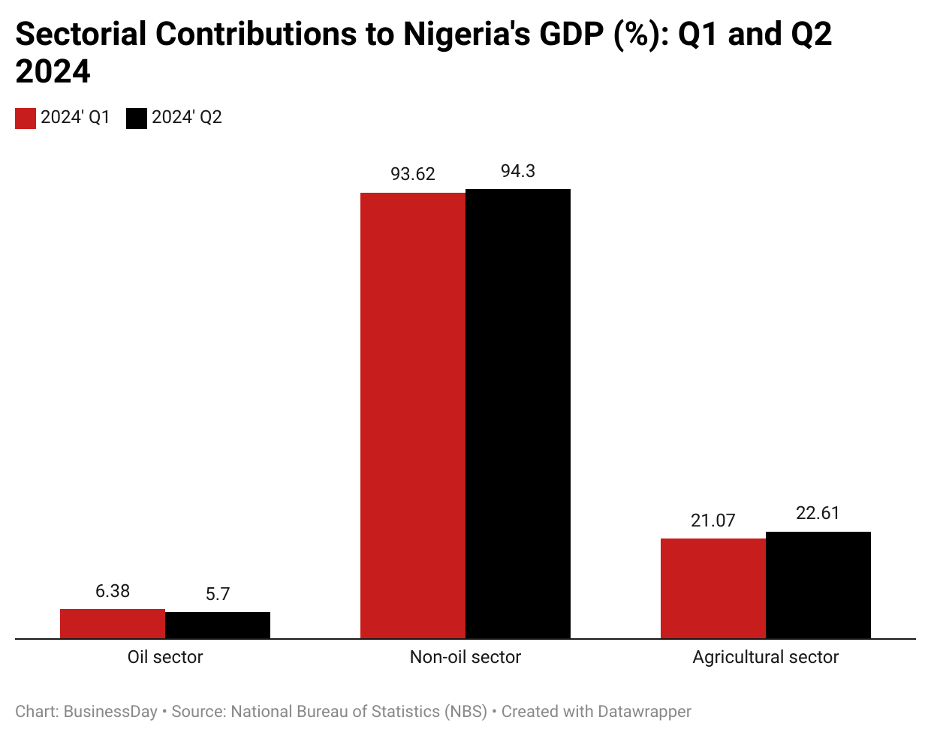

According to the NBS’ GDP report for Q2, besides the services sector which contributes the most to the economy with 58.76%, the agricultural sector follows with 22.61%.

“The nation’s Agricultural sector has consistently contributed the largest to the country's GDP thus proven to be resilient and resistant to economic and oil price shocks,” CFG Advisory noted in a recent report.

The CPPE chief further said that efforts must be made to reduce the issue of logistics as it affects the level of productivity.

He stated that if productivity improves, the exchange rate will be stabilised while exports will grow, giving a glimmer of hope to hitting the one trillion dollar goal.

“Look at these domestic refineries, if we're able to get it right, the pressure on the naira for imports of fuel will reduce. There are potentials to make it happen,” Yusuf said.

As part of efforts to reach a $1 trillion economy, Nigeria targets an oil production of two million barrels per day by 2025 and is intensifying efforts to diversify the economy.

With the Port Harcourt, Warri, and Kaduna refineries yet to recommence operations, the Dangote refinery is tipped to boost the Nigerian economy.

The refinery projects a turnover of $30 billion in the next two years. This is even as more domestic refineries are expected to become operational before 2030.

Non-oil revenues to the rescue?

Beyond proceeds from oil revenues, experts have also advised that the government should diversify more into non-oil sectors such as real estate and agriculture to hit the trillion dollar goal.

“The goal is more than achievable as soon as 2025 if Nigeria is ready to offer enough immediate opportunities for foreign investments in government owned companies, real estate, and infrastructures, like India and Saudi Arabia are doing,” Teriba said.

The Central Bank of Nigeria's recapitalisation rule is another effort by the government to ensure stability of the country's banking sector and drive a trillion dollar economy with a total N4.14 trillion expected to be raised in 2026.

“With the proposed recapitalisation exercise, the prospect of a reduction in the number of banks is high. However, this reduction will create room for an even stronger banking sector that can drive a USD1trn economy by 2030,” Deloitte, a UK-based professional services firm, said in a report.