Whenever the issue of tax increases arises, I’m reminded of a story from the book Why Nations Fail: The Origins of Power, Prosperity, and Poverty, by Daron Acemoglu and James A. Robinson.

The Kingdom of Kongo during the 16th and 17th centuries imposed arbitrary taxes. One such absurd tax was levied every time the king’s beret fell off. These taxes, along with forced labour on plantations, discouraged the people from investing in their productivity. They were aware that any additional wealth they created would be seized by the ruling elite, so they avoided the market altogether to escape plunder.

Any government that seeks to foster prosperity among its citizens must reject taxation systems that stifle economic development and investment while failing to provide essential public goods or infrastructure in return.

The Origins of Modern Income Tax

In 1799, William Pitt introduced the first modern income tax in the United Kingdom as a temporary measure to fund the Napoleonic War. It was levied at 10% on incomes over £60, marking a turning point in fiscal history. Since then, taxation has become an essential tool for funding social services, transforming economies, and protecting the poor from economic challenges.

Bola Tinubu's Tax Reforms: A Success Story in Lagos

During his tenure as Governor of Lagos State from 1999 to 2007, President Bola Tinubu was instrumental in reforming the state’s tax system. The state’s internally generated revenue (IGR) surged from a monthly average of ₦1.22 billion in 1999 to ₦6.9 billion in 2007. By 2022, Lagos was generating a remarkable ₦54.3 billion monthly in tax revenue.

Tinubu has pledged to replicate this success at the federal level, and in 2023, he established the Presidential Special Committee on Tax Reform, led by Taiwo Oyedele. This committee has been working to overhaul the nation’s tax structure and has made several recommendations to both the presidency and the National Assembly.

A Complicated Tax System: Nigeria’s Tax Burden

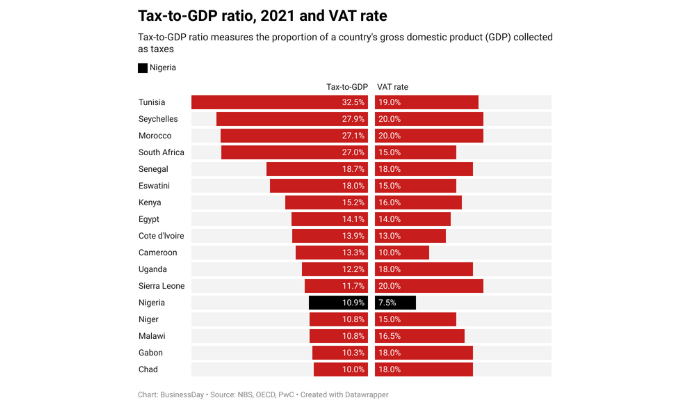

Despite efforts to reform, Nigeria’s tax system is burdened by complexity, with over 60 official taxes and more than 200 unofficial ones. While the country’s tax-to-GDP ratio is only 10.9%, other African countries such as Tunisia (32%), South Africa (27%), and Kenya (15.2%) have higher ratios. Nigeria also has one of the lowest VAT rates in Africa at 7.5%, compared to Tunisia (19%), South Africa (15%), and Kenya (16%). This situation has contributed to recurring revenue shortfalls, forcing the government to rely on borrowing to finance its budget.

Implications of Low Tax Revenue: Infrastructural and Social Deficits

The government’s inability to collect sufficient tax revenue has dire implications. It has resulted in an inability to fund essential social services and infrastructure, limiting the state's capacity to provide public goods. In a country where public services are scarce, this is a critical issue.

When governments do not collect what is optimal from the economy, it becomes nearly impossible to provide for their citizens. Nigeria’s low tax collection is mirrored by its low government expenditure-to-GDP ratio, which further exacerbates the problem of poverty and infrastructure deficits.

Efficiency in Taxation: A Core Principle Lacking in Nigeria

A key principle of taxation is efficiency, which Nigeria’s tax system lacks. Taxpayers, including contractors, are often overcharged, and obtaining refunds is notoriously difficult. The new proposed tax law aims to address these inefficiencies by reducing the number of taxes and simplifying the overall system, allowing taxpayers to pay what is required by law, without unnecessary complications.

The New Tax Law: What to Expect

The new tax law proposed by the Presidential Special Committee on Tax Reform is aimed at simplifying Nigeria’s convoluted tax system. If passed, the law could consolidate the 60+ official taxes down to just 6 or 8, reducing the tax burden on ordinary Nigerians.

Notably, items essential to daily life such as raw food, and semi-processed foods including bread, rent, public transport, education, and healthcare would be exempt from VAT. This provision would relieve the poor from bearing the brunt of tax-related price increases on essential goods and services.

Employees whose monthly income is less than or equal to N1.5 million per month will also be exempted from personal income tax.

VAT Changes and Relief for Businesses

The middle class, however, will see an increase in VAT, rising from 7.5% to 10% by 2025, and possibly to 15% by 2030. The VAT refund process will take between 30 and 60 days, without the need for an audit.

For businesses, the new law offers several advantages. Businesses with an annual turnover of ₦50 million or less will be exempt from company income tax, small businesses will be exempted from VAT, personal income tax of their employees, and withholding tax.

Additionally, businesses will receive tax relief if they provide transport for their employees or employ more workers than they would normally do for an average of 3 years. The company income tax rate is also set to drop from 30% to 25% over the next two years.

Simplifying Corporate Taxation

The new law also proposes merging the Education Tax, IT Levy, Police Fund Levy, and NASENI Levy into a single 4% tax, with the potential to lower it to 2% in the future. Businesses will benefit from this simplified tax structure, and those operating in priority sectors will get tax relief if certain investments are met for a particular time.

States Must Live Up to Expectations

Under the new tax system, if implemented, the VAT sharing formula will be restructured, allocating 90% of VAT revenue to state and local governments, while the federal government will receive only 10%. This is a shift from the current arrangement, where 85% goes to states and local governments, and 15% to the federal government.

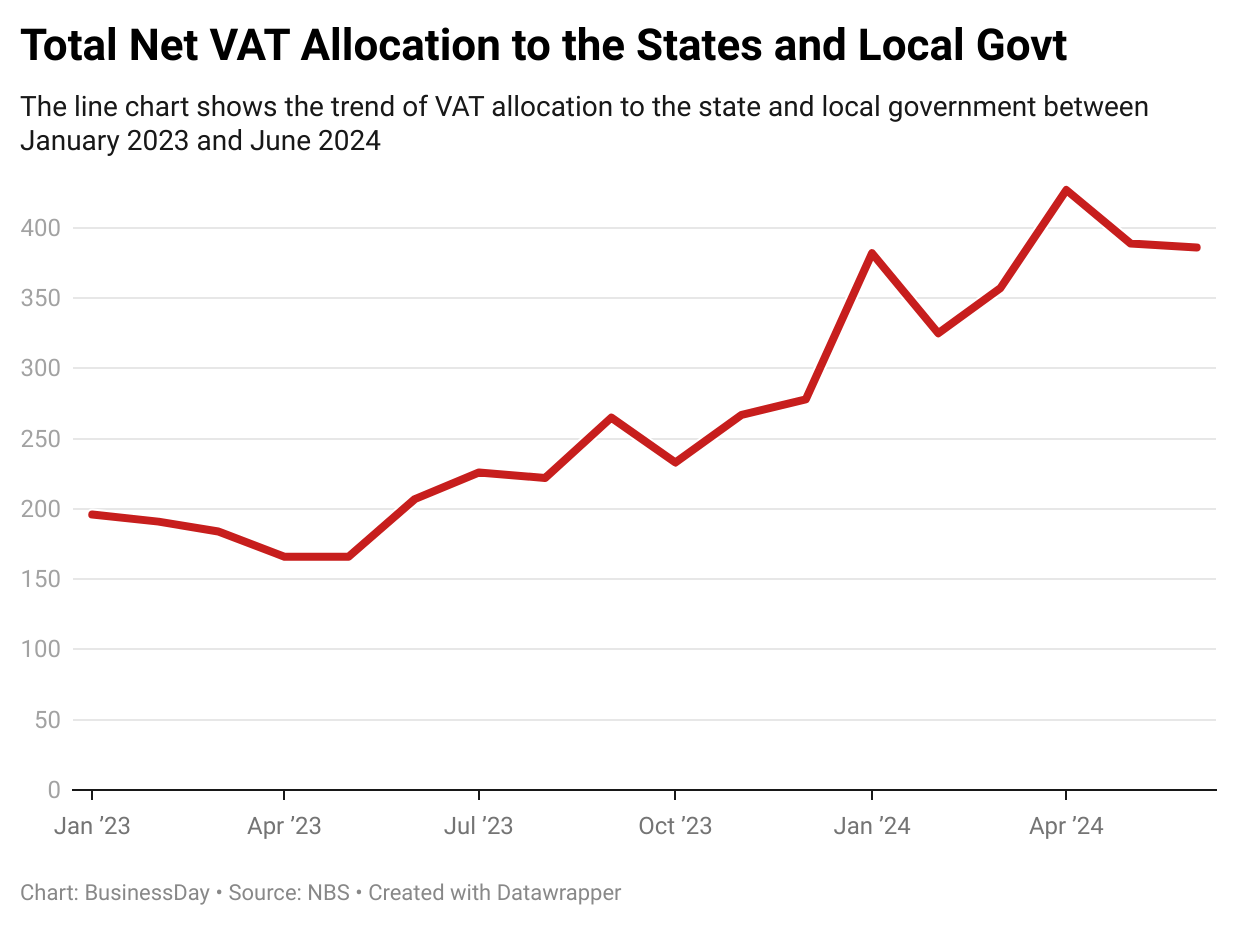

Despite fluctuations in VAT revenue earlier in 2023, such as declines in February and April, there was a notable surge of 25% in June 2023 and another increase of 38% in January 2024. These spikes can be attributed to two key factors: the June VAT revenue was generated before the removal of fuel subsidies, while the January 2024 revenue was influenced by festive spending in December 2023.

Overall, VAT revenue has been on an upward trend, likely due to inflation, as VAT is tied to the price of goods and services.

With a larger share of VAT revenue going to the states and local governments, there is a greater responsibility on them to use these funds effectively. The money collected from citizens must be reinvested into public goods and services. Otherwise, as seen in the earlier example of the Kingdom of Kongo, taxation without corresponding benefits can lead to widespread dissatisfaction and hinder economic growth.

The Role of Digitalisation in Tax Collection

Another significant reform is the planned digitalisation of tax collection. This change aims to phase out cash transactions and eliminate informal tax collectors, such as the notorious "Agberos" who levy unofficial taxes on transporters. Farmers, who often face multiple informal levies as they transport goods to market, are also expected to benefit from this reform. The question is how this is going to be implemented because this seems to be a national malady.

Potential Challenges: Fiscal Drag and the Cobra Effect

However, the government must be cautious about the risks associated with fiscal drag, where inflation or income growth pushes taxpayers into higher brackets without a corresponding rise in purchasing power. This phenomenon could increase the tax burden on the middle class and undermine the progressive nature of the new system.

Additionally, the government should avoid the "cobra effect"—where an attempted solution to a problem ends up making the problem worse. Removing taxes from the poor is a positive step, but the government must ensure that this does not lead to revenue shortfalls that hinder economic development.

A Balance Between Fairness and Fiscal Responsibility

The new tax law seeks to balance fairness and fiscal responsibility by reducing the tax burden on those who can least afford it while ensuring that wealthier individuals and businesses contribute their fair share. If implemented effectively, it could relieve overtaxed individuals and businesses, while increasing government revenue in the long run.

Conclusion: A New Era for Nigeria’s Tax System?

In summary, the proposed tax law has the potential to reshape Nigeria’s fiscal landscape by reducing the tax burden on the poor and simplifying the system for businesses. However, careful implementation is crucial to avoiding unintended consequences and ensuring that the reforms lead to long-term improvements in tax revenue, economic growth, and social welfare.

Oluwole Crowther is an Economic Research Analyst, with a BSc in Economics and an MSc Economics in view at the University of Ibadan.